I think I got a clear steer on areas for innovation at Next Bank Europe in Barcelona, and you won’t be surprised to discover that the top ones are all related to identity, not money.

Well, the lovely people at Next Bank Europe 2014 (#NBEU14) invited me down to the lovely city of Barcelona to take part in their September event and it was well worth the trip. Apart from catching up with some old fintech friends, always the most enjoyable part of any trip, and meeting some new people, something I always enjoy, it was interesting to see the fintech startup scene from a different perspective.

The reason that the #NBEU14 folks asked me to come along was to have an onstage discussion with Forum friend Jon Matonis, now of the Bitcoin Foundation, in order to educate the audience about the state and potential of bitcoin and associated technology. Now, I had noticed a tweet from Sam Maule in which he said that the stage looked like his daughter’s bedroom: there was sofa and a couple of chairs and a table and stuff all around. During the morning panel, it had occurred to me that the panelists weren’t really using the set, they were just sitting on the chairs and answering questions as if they were lined up on normal conference chairs. So that gave me an idea.

As we came to the end of the coffee break, I went over to Jon (who was expecting a conventional Q&A session) and said words to the effect of “just go sit on the sofa and we’ll be two old guys having an argument”. Jon, who is a great sport, said OK. We went up on stage and Jon sat back on the sofa. I sat down casually in one of the chairs and, began casually leafing through a copy of The Economist, before casually remarking on the XBT price. From there on, things gradually escalated into an all-out argument on stage.

We ignored the audience completely and got into it. Jon is a smart guy, and in my experience arguing with smart people is a pretty efficient method of learning, so I enjoyed every moment of it. I could see the countdown clock out of the corner of my eye, but the audience could not, so I kept the debate going until I saw the clock hit zero, at which I point I put down the microphone and somewhat over-theatrically flounced off stage!

Now, as it turned out, this fireside chat greatly exceeded expectations and, if Twitter reaction is anything to go by, the delegates really appreciated this rather different approach to the traditional managed Q&A session on new technology.

The choice before Bitcoin users is not whether they should want regulation, but what to do about it.

As the digital currency Bitcoin continues to grow and evolve, regulators are taking notice. From anti-money-laundering rules issued by the Treasury Department in March, to reports that the Commodities Futures Trading Commission is "seriously" examining the currency, to a recent Government Accountability Office recommendation that the IRS issue guidance on Bitcoin-related income reporting, government seems to be getting serious. The question for the largely libertarian Bitcoin community is, should it engage those regulators or ignore them?

Ignoring the regulators, perhaps with middle fingers firmly extended, is an option, some argue, because Bitcoin is a decentralized peer-to-peer network with no centralized point of control. It exists outside of government or corporate control and can't be easily shut down or controlled. This is what attracts many to the currency, especially a large contingent of crypto-anarchists who made up Bitcoin's earliest adopters and boosters.

As Jon Matonis, the incoming executive director of the Bitcoin Foundation has put it, attempting to regulate Bitcoin would be like trying to regulate the specifications of air guitars. But he points out that while the protocol itself can't be touched, there are centralized points of control in the Bitcoin ecosystem susceptible to regulation: the exchanges that allow one to trade bitcoins in and out of national currencies. Indeed, they are the targets of the money-laundering rules that require firms to report on their customers.

This doesn't concern those who see Bitcoin as a way to completely opt out of state control, however. After all, if you're trying to escape the legacy banking system and government fiat currencies, interfacing with that system is more than a little beside the point. Even if exchanges were to be shut down in the U.S. for regulatory non-compliance, they could prosper in freer jurisdictions, and ultimately the goal for many is to be able to operate on bitcoins alone so that exchanging ceases to be a concern. So, many argue, there's no point in going along with regulation.

"The solution is to create decentralized exchanges and to promote business models and closed-loop paradigms that make fitting into the current institutional structure irrelevant," Matonis says. "It is a perpetually losing battle to seek minor legal victories within the confines of an arbitrary, subjective court system."

With the rapid growth of Bitcoin and the proliferation of cryptocurrency exchanges, it’s easy to forget that a mere 12 years ago, there were no trading markets for Bitcoin and no market established Bitcoin prices.

In fact, following the mining of the first Bitcoin block on 3 January 2009 by the eponymous Bitcoin creator Satoshi Nakamoto, it would be another 9 months until the first known Bitcoin price was recorded on 5 October 2009.

Some common themes among the early Bitcoin exchanges were that they were operated more or less as one man outfits, they quoted extremely low Bitcoin prices, the exchanges had limited interest even among the Bitcoin hobbyists, and the exchanges were prone to attacks from hackers and fraudulent activity.

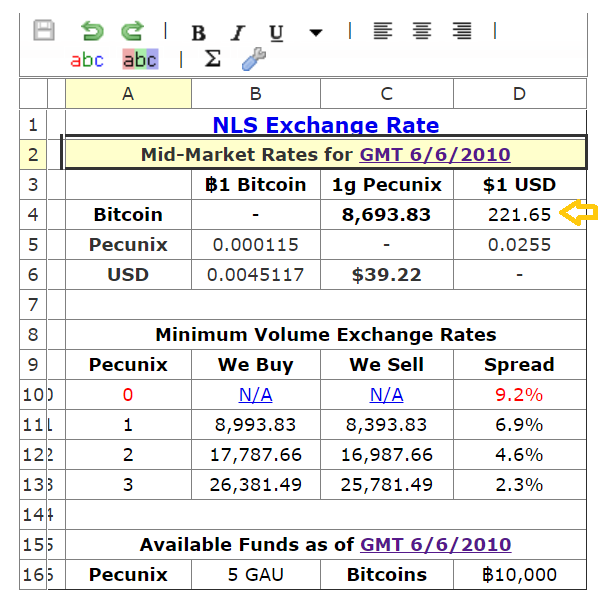

New Liberty Standard (NLS)

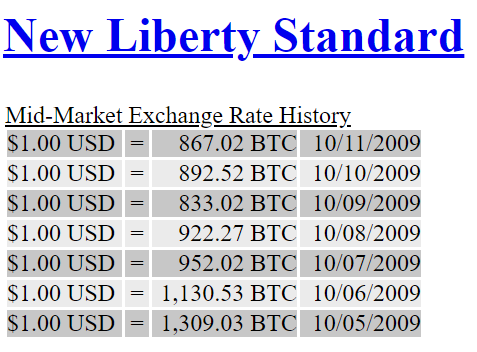

The first known Bitcoin price, or exchange rate, recorded on 5 October 2009 was published on what was the world’s first Bitcoin exchange site, New Liberty Standard (NLS), a site which offered a service to buy and sell Bitcoins in exchange for US dollars using PayPal. The site was operated by “NewLibertyStandard”, who was a frequent contributor to the early Bitcoin forum Bitcointalk.org, and who discussed his exchange site on the forum in posts such as here.

The very first Bitcoin / USD exchange rate published on the New Liberty Standard site on 5 on October 2009 was USD $1.00 = 1,309.03 BTC, which equated to an incredible $0.00764 per Bitcoin, or in other words 7.6 US cents per 100 Bitcoins.

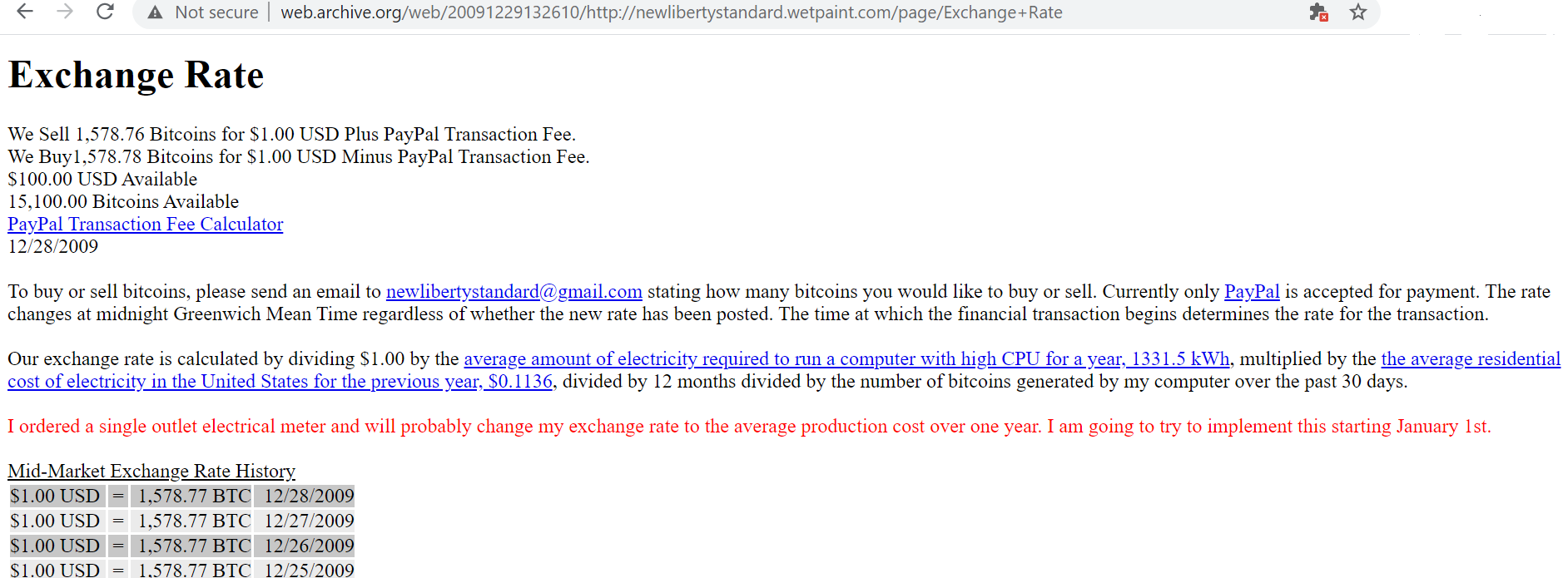

NewLibertyStandard calculated this exchange rate using a formula based on:

“dividing $1.00 by the average amount of electricity required to run a computer with high CPU for a year, 1331.5 kWh, multiplied by the average residential cost of electricity in the United States for the previous year, $0.1136, divided by 12 months divided, by the number of bitcoins generated by my computer over the past 30 days.”

New Liberty Standard’s first Bitcoin / USD prices, 5th – 11th October 2009. Initial price 1,309.03 BTC per USD

As you can see, this Bitcoin price in the early days was determined not by buying and selling activity of Bitcoins, but by the price of electricity and the site owner’s personal Bitcoin mining output. The calculation became a bit more complicated in early 2010 using rolling averages and the addition of broadband internet costs, and can be seen in another archive imprint from the New Liberty Standard site in late April 2010 here.

A list of the daily USD / Bitcoin prices between 5 October and 28 December 2009 can be seen on a 29 December 2009 Wayback Machine (Archive.org) imprint of the New Liberty Standard exchange rate page here. If the Wayback Machine page is slow to load, these historic exchange prices can also be seen on NewLibertyStandard’s webpage here.

28 Dec 2009: NLS quoted that it would sell 1,578.76 Bitcoins for US$ 1.00 plus a Paypal transaction fee.

The best rate quoted for buying Bitcoins on the NLS exchange in 2009 was on 17 December 2009 when you could buy an incredible 1630.33 BTC for US $1.00.

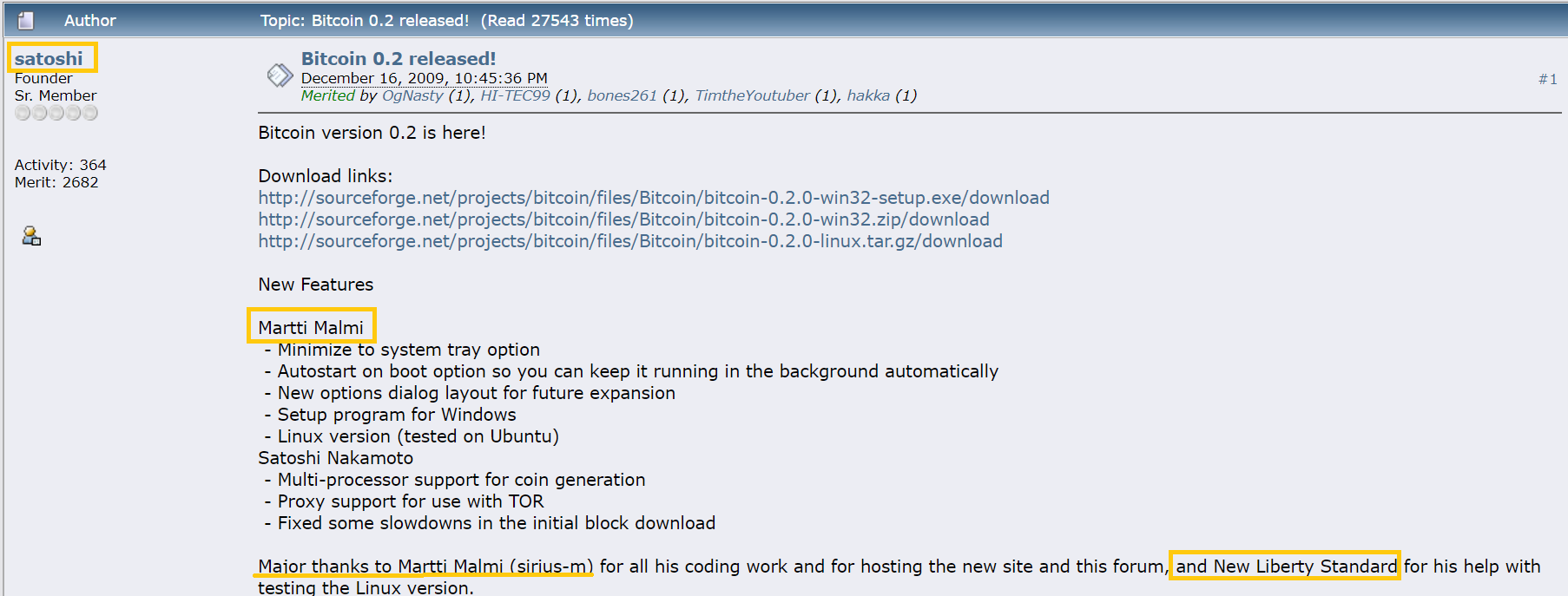

NewLibertyStandard was also known to Satoshi Nakamoto, as for example, Satoshi thanked NewLibertyStandard on 16 December 2009 for helping to test Bitcoin 0.2 (see Bitcointalk discussion topic here).

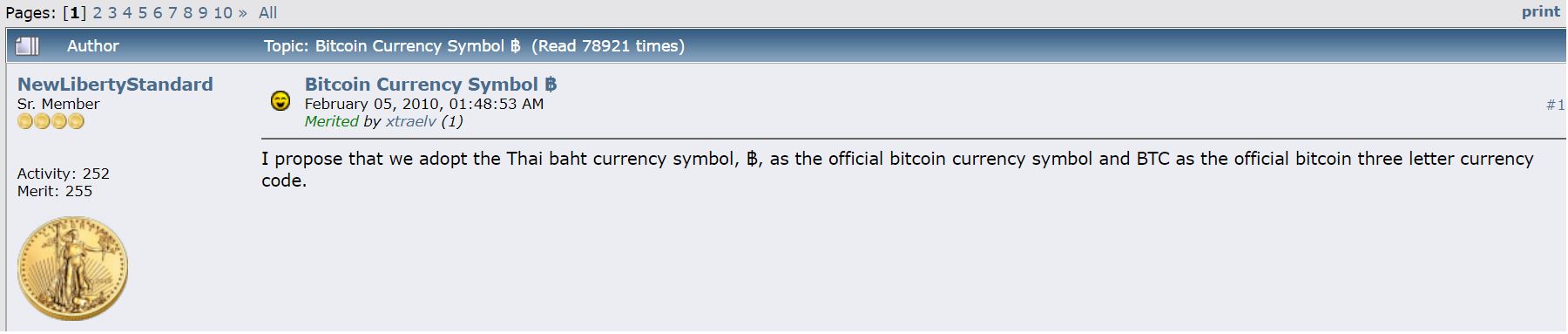

Interestingly, it was NewLibertyStandard who came up with the Bitcoin symbol ฿ and the Bitcoin ticker BTC, when on 5 February 2010 he posted on the Bitcointalk.org forum that:

“I propose that we adopt the Thai baht currency symbol, ฿, as the official bitcoin currency symbol and BTC as the official bitcoin three letter currency code.”

NewLibertyStandard proposes BTC ticker code and Thai baht ฿ for use as Bitcoin symbol

In early October 2009, there was also an historic Bitcoin / USD transaction which consisted of a Finnish programmer and early Bitcoin supporter named Martti Malmi selling 5050 BTC to NewLibertyStandard for US$ 5.02, which was the equivalent of 9.94 US cents per 100 Bitcoins.

This transaction is confirmed by a Tweet on Martti Malmi’s Twitter account as below

This transaction was, as Malmi explains below, to help support the Bitcoin trading service of New Liberty Standard.

Malmi also interestingly went on to launch his own Bitcoin for fiat currency exchange service for a time in 2010, which he called bitcoinexchange.com. Although there are no Archive.org imprints of this site, Malmi (who went by the name Sirius in the Bitcointalk,org forum) discusses it in January 2010 here, and also mentioned it last month (December 2020) in a Tweet below:

Not only was Martti Malmi known to Satoshi, but be also helped Satoshi code and test Bitcoin 0.2, as can be seen from this Bitcointalk posting on 16 December 2009 here.

Satoshi Nakamoto thanks Martti Malmi and NewLibertyStandard for their help with the Bitcoin 0.2 release, 16 December 2009

By 19 January 2010, the New Liberty Standard exchange was seeing a small volume of business, as attested by the site owner NewLibertyStandard in a post on Bitcointalk.org:

“I have had people buy bitcoins from me and sell bitcoins to me. Supply and demand, albeit only a small amount, already exists and is all that is really needed. Offering to exchange bitcoins for another currency is ultimately no different from exchanging bitcoins for goods or services.”

Exchange rate of 221.65 BTC per $ 1.00 on the NLS exchange, 6 June 2010

On his website, NewLibertyStandard descried Bitcoin as an “economic revolution”, saying that “Bitcoin is the gold standard of digital currency. The availability of bitcoins cannot be manipulated by governments or financial institutions and bitcoin transactions occur directly between two parties without a middleman.”

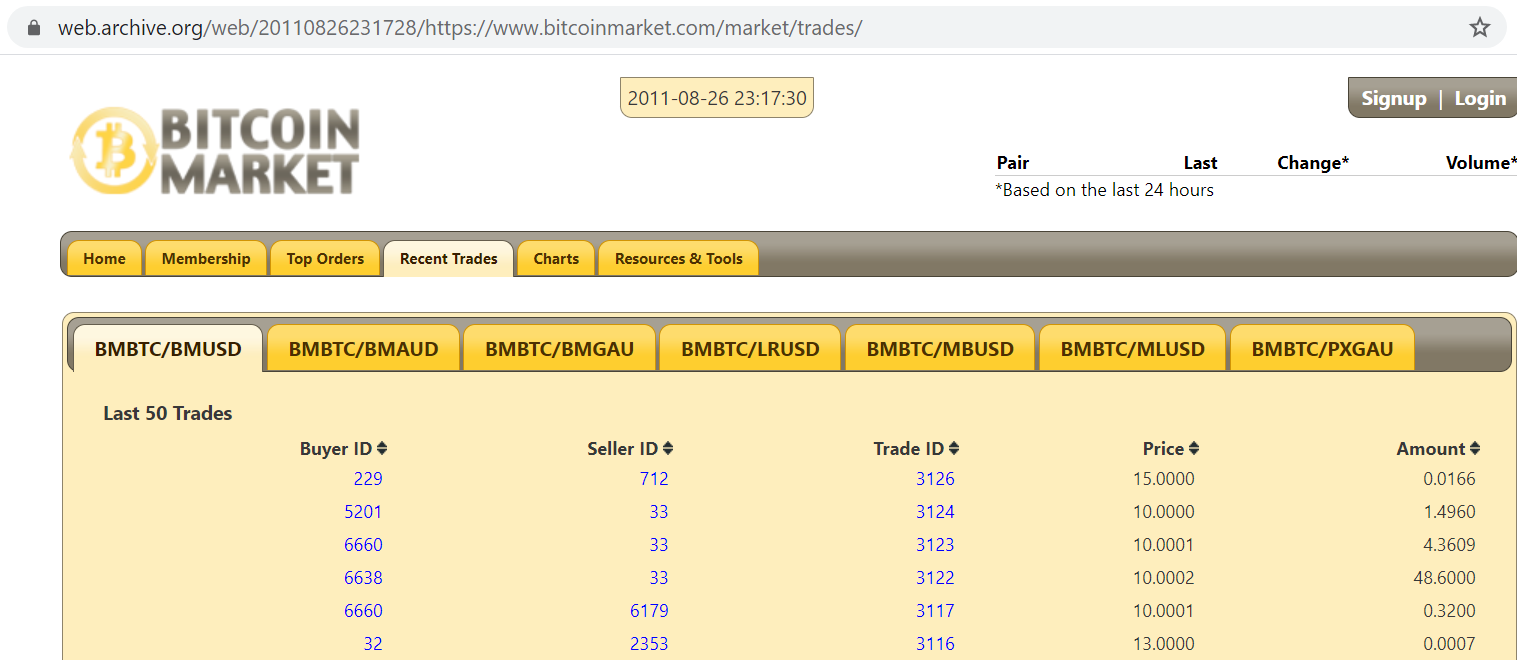

Bitcoin Market (BCM)

The second pioneering initiative to create a price for Bitcoin also came from someone who became a well-known contributor to the Bitcointalk.org forum. This was a Bitcoin exchange site called Bitcoin Market (www.bitcoinmarket.com), created in early 2010 by Bitcointalk’s ‘dwdollar’, whose real name ironically is Dustin Dollar.

Website imprint of the bitcoinmarket.com Bitcoin exchange on 26 August 2011, price $10 – $15 per BTC

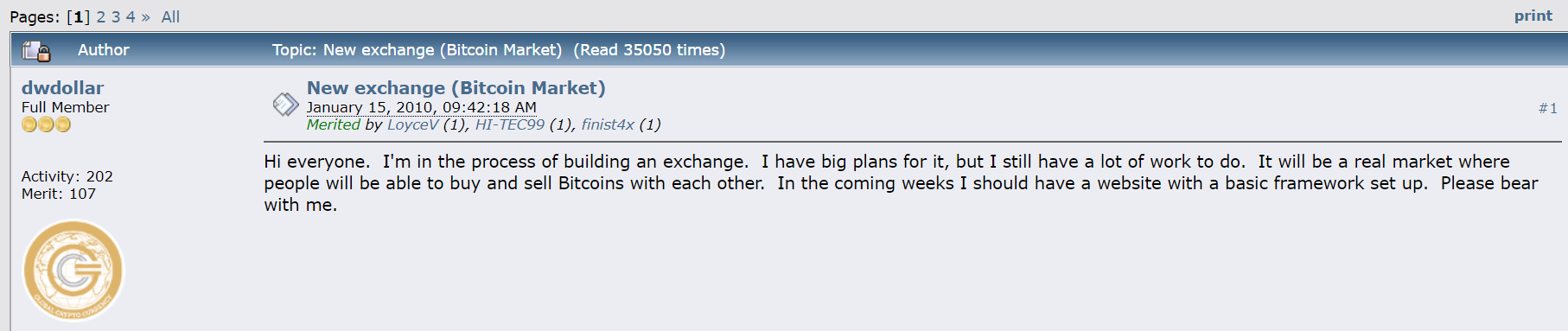

The very first post of ‘dwdollar’ on Bitcointalk.org was to announce his plans to create a Bitcoin exchange, when he posted on 15 January 2010:

“Hi everyone. I’m in the process of building an exchange. I have big plans for it, but I still have a lot of work to do. It will be a real market where people will be able to buy and sell Bitcoins with each other. In the coming weeks I should have a website with a basic framework set up. Please bear with me.”

dwdollar’s announcement of Bitcoin Market on 15 January 2010

Again on 6 February 2010 in an update he added that:

“I am trying to create a market where Bitcoins are treated as a commodity. People will be able to trade Bitcoins for dollars and speculate on the value. In theory, this will establish a real-time exchange rate so we will all have a clue what the current value of a Bitcoin is, compared to a dollar. I have an early version up at http://98.168.168.27:8080/”

‘dwdollar’ was adamant that the exchange should reflect real trading between market participants and not the production costs of Bitcoin:

“Unless there is a way to determine demand, no one will be using them as a currency. Even now, every Bitcoin has a value. The key is finding it and tracking it.

I want this to be a real market where buyers and sellers determine the value based on their demand. It will match buyers and sellers (it can already do that) accordingly. I will only be a broker. I don’t think we should be worried about what the value is.

Our main concern should be accurately determining that value as it fluctuates…. The fact we are worrying about people dumping Bitcoins suggests we haven’t determined an accurate value yet."

The Bitcoin Market (a.k.a. BCM) site went live in March 2010 and used PayPal for cash handling (also adding Pecunix gold grammes (GAU) and Liberty Reserve (USD) at later dates). On 16 March 2010, dwdollar posted on the Bitcointalk.org forum saying that he had:

“created an account and placed a bid for 500 Bitcoins @ $.0067/BC which I think is NewLibertyStandard’s current exchange rate.”

This 16 March 2010 rate of $0.0067 per coin, which was 67 cents for 100 coins, was 8.77 times more than the NewLibertyStandard’s starting price that had been specified on 5 October 2009, less than 6 months earlier.

On 17March 2010 (St Patrick’s Day), dwdollar posted another message that:

“There are 9 people signed up but only 3 have made a deposit so far. Myself makes 4. Looks like we had our first real trade around noon!”

Interestingly, a few days later on 20 March 2010, there was a reply to dwdollar’s post on the Bitcointalk.org forum from the now famous (in the cryptocurrency world) Jon Matonis, who said:

The blog focuses on digital online exchangers and anonymous digital currencies penetrating the market so that we may all protect our financial privacy. Should be interesting and entertaining for many on this forum.”

Bitcoin Market in its ‘About page" claimed that “it was the first to offer a free-floating exchange rate and an escrow trading system.” It incorporated as Bitcoin Market LLC in September 2010. A new site Bitcoin Market site was rolled out in October 2010 with Dustin Dollar (a.k.a dwdollar) as the “developer of the Bitcoin Market website and owner of Bitcoin Market LLC.”

The earliest captured imprint of the site via the Wayback Machine is September 2011 and can be seen here. Some Bitcoin Market trades (from 26 August 2011) can be seen on an archived page here, where prices by then had reached the range of $10 – $17 per Bitcoin.

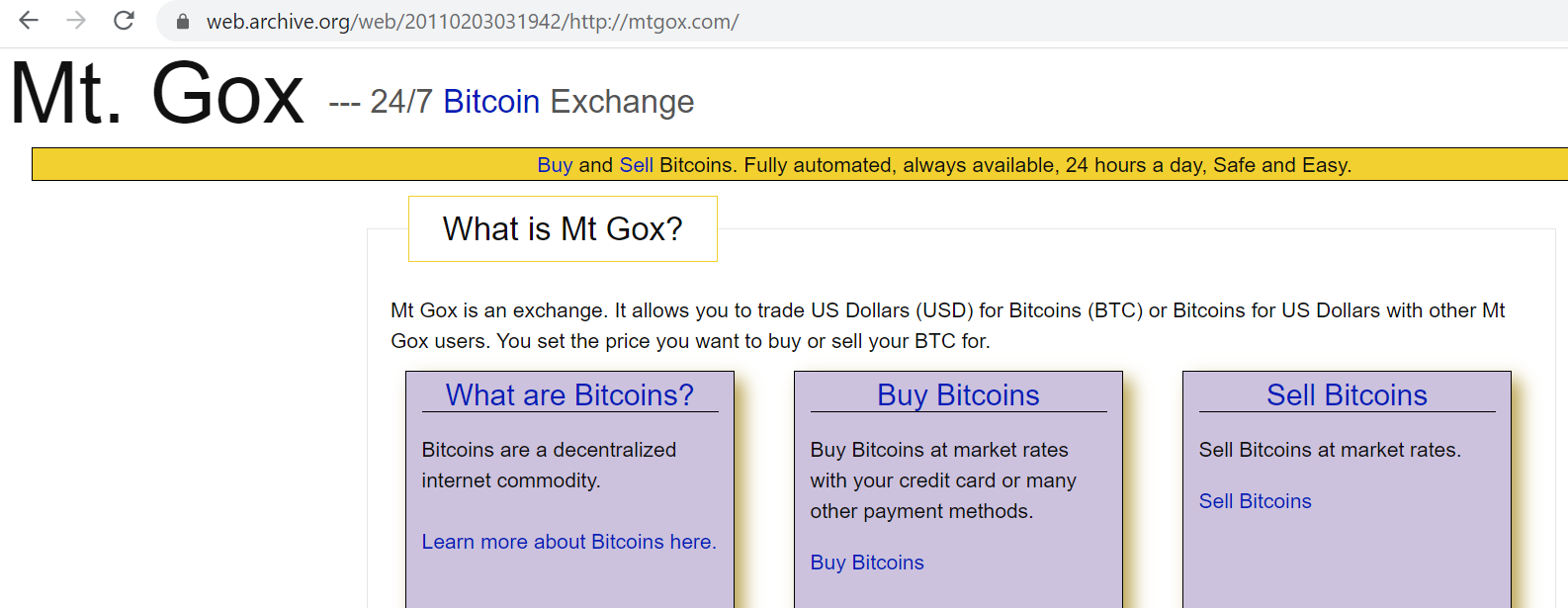

Mt. Gox

Following the launch of Bitcoin Market in March 2010, the next major development for Bitcoin Exchanges came a few months later with the launch of the now famous (and infamous) Mt. Gox on 18 July 2010, which described itself as an exchange that “allows you to trade US Dollars (USD) for Bitcoins (BTC) or Bitcoins for US Dollars with other Mt Gox users. You set the price you want to buy or sell your BTC for.”

Launched by Jed McCaleb, the exchange and website name is an abbreviation of a previous site of McCaleb’s called “Magic: The Gathering Online”, hence the name Mt Gox. McCaleb would later reach fame as the co-founder and CTO of Ripple, and the co-founder of Stellar (where he is also currently CTO).

McCaleb announced the launch of his exchange on, you guessed it, the Bitcointalk.org forum, in a short post here, where he said:

“Hi Everyone, I just put up a new bitcoin exchange. Please let me know what you think. https://mtgox.com“

Screenshot of Mt. Gox Bitcoin exchange homepage from 3 February 2011, one week before BTC reached parity with the US dollar.

The prices on Mt Gox were basically in the form of last traded price, High, Low and volume (over 24 hours), as well as Current Lowest Buy and Current Highest Sell Prices offered by exchange users. According to the Mt Gox homepage, “all trades are between users. So the current buy price and current low price is just what someone else entered.”

An early website imprint of the Mt. Gox home page from 3 February 2011 can be seen here.

An archive imprint of a page from website Bitcoin Charts (bitcoincharts.com) on 19 November 2010 shows Bitcoin prices in US dollars for both Bitcoin Market and Mt Gox, with the BTC price in US dollars in a range from $ 0.23 to $0.28 per Bitcoin.

There was even technical analysis of the Bitcoin price on the Mt Gox site from as early as November 2010, with user ‘S3052’ (who was also active on Bitcointalk.org) posting daily updates, such as on 6 December 2010. In hindsight, these Bitcoin prices look miniscule now and practically unbelievable:

“Overall, the decline is continuing. Unless 0.3 – 0.35 $ are taken out substantially, the trend is DOWN. A strong target remains 0.1 – 0.14 $.

Analysis

1. Long term outlook: BTC/USD have broken the long-term trendline (now around 0.23 $ and slowly rising) to the downside. Support lies in the 0.11-0.14 $ area. As long as prices find support there, there is “light in the end of the tunnel”, meaning an end of the decline with continued rally.

2. Short term update “A break down below 0.20 would deteriorate the technical picture heavily and open the door for fast declines”. We have breached the 0.20 level with a low of 0.185 $ today, so unless prices move back above 0.20 and more importantly, the trendline quickly, a sell off towards ultimately 0.1 $ is quite probable. As you can see in the volume picture, huge buying volume came in between 0.09 and 0.10 $, which makes this a likely strong support level.

Less than a month later, Bitcoin prices had rallied nearly 500% as a range of prices on the Mt. Gox ‘Buy Bitcoins’ page (3 January 2011) were in the range of US$ 0.93 to US $ 0.955 per Bitcoin.

In March 2011, Jed McCaleb sold the Mt. Gox Bitcoin exchange to Mark Karpelès (who went by the name MagicalTux on Bitcointalk.org). The sale was announced on the Bitcointalk.org forum on 6 March 2011 by user mtgox (Jed McCaleb) where he posted:

“Hello Everyone

I created mtgox on a lark after reading about bitcoins last summer. It has been interesting and fun to do. I’m still very confident that bitcoins have a bright future. But to really make mtgox what it has the potential to be would require more time than I have right now. So I’ve decided to pass the torch to someone better able to take the site to the next level.

MagicalTux has already contributed a lot to the bitcoin community and in many ways he will be better at running the site than I was.

…Thanks to everyone that has supported mtgox so far. Can’t wait to see BTC hit $10! “

Interestingly, Mark Karpelès became one of the founding member of the Bitcoin Foundation when it was established on 23 July 2012, along with such names as Roger Ver, Gavin Andresen and of course Satoshi Nakamoto.

Founding members of the Bitcoin Foundation, established 23 July 2012. Source

Following the sale, Karpelès, who had moved from France to Japan in 2009, moved the Mt Gox operation to the Shibuya business district in Tokyo and structured Mt. Gox as part of his Japanese company Tibanne Co Ltd. A revamped Mt. Gox website was launched on 1 December 2011. See press release here.

Homepage of the Mt. Gox Bitcoin exchange after it had moved to Japan

By that time, Mt Gox described itself as “facilitating the exchange of Bitcoins between users globally in the currency of their choice. Multiple currency markets allow users to purchase and resell their Bitcoins in up to 16 different currencies, along with the ability to securely store Bitcoins in a virtual “vault” for safe keeping”

The revamped Mt. Gox website from late 2011 can be seen here in a Wayback machine archive imprint from 11 January 2012, where the prices at that time were – Last price: $6.849. High: $7.138. Low: $6.500. Volume: 100,958 BTC, Weighted Avg Price:$6.84563

Bitcoin price chart in USD, MTGOX 2012 March – April. Price range $4.50 – $5.50 Source: Mt. Gox archive website

The rest, as they say is history. For anyone not aware of what happened to Mt. Gox, it filed for bankruptcy on 28 February 2014, citing insolvency and seeking protection from creditors, announcing that it had lost approximately 850,000 Bitcoins. This comprised 750,000 Bitcoins belonging to clients and 100,000 Bitcoins belonging to Mt. Gox. Mt Gox claimed it had been hacked and the Bitcoins stolen.

According to the Wall Street Journal as cited by the LA Times:

‘“There was some weakness in the system, and the bitcoins have disappeared. I apologize for causing trouble,” said Mt. Gox Chief Executive Mark Karpeles at a news conference in Tokyo.’

A few weeks later, Mt Gox said that it ‘found’ 200,000 Bitcoins after it was pointed out by blockchain watchers that these coins were still moving among Mt Gox BTC addresses. For a good recap about Mt Gox at the time see a March 2014 article from Wired here.

According to the Japan Times, a US task force investigating Mt Gox traced the bulk of the 600,000 hacked Bitcoins to a Russian programmer called Alexander Vinnik and arrested him in Greece in 2017 for “allegedly laundering funds From hack Of Mt. Gox”. Vinnik had been the co-founder of an early Russian Bitcoin exchange in 2011 called BTC-e (old site here). Not to be confused with another early Russian Bitcoin exchange (also started in 2011) called BTCex (old site here).

Conclusion

Looking back on the pioneering Bitcoin exchanges, its hard to believe that it was less than 12 years ago. In some ways, these early Bitcoin exchanges of New Liberty Standard, Bitcoin Market, and Mt. Gox even look like they are from a bygone era. It wasn’t that the technology didn’t exist in 2009 – 2011 to create robust, sophisticated and secure Bitcoin exchanges. Its just that there was no institutional interest and investment to do so.

Hence, the pioneering exchanges were launched by a smattering of interested individuals who were enthusiastic and active in the Bitcoin space at that time. Its striking also that the main players in this drama all knew each other in one way or other, that they believed in sound money that cannot be inflated, and that many of them are still major figures in the cryptocurrency world.

While the prices established for Bitcoin during those times, from 1500 BTC for a $1 in October 2009 to even 1 BTC for $1 in February 2011, are historically interesting, maybe the more lasting contribution of these early exchanges is that they paved the way for the massive and ever accelerating crypto ecosystem which has been built on their foundations.

California's message to Bitcoin supporters: if you "may be" doing the crime, we'll tell you what you'll do in hard time.

The California Department of Financial Institutions' cease and desist order dated May 30 wasn't as explicit in implicating the Bitcoin Foundation, a nonprofit with a mission to standardize and promote the Bitcoin technology, of any legal wrongdoing as it was in outlining punitive consequences if the electronic currency advocacy group was to be transmitting money without licenses or the state's authorization. Jon Matonis, who sits on the Board of Directors for Bitcoin Foundation, brought California's order to attention in a column for Forbes published yesterday.

The Bitcoin Foundation’s executive director, Jon Matonis, travels the world to promote the virtual currency as a replacement for traditional money. Some of his members want him to focus on a less lofty goal: helping them make lots of old-fashioned cash.

Matonis, a longtime advocate of what he calls “non- political money”, has built the group into a kind of a bitcoin governing body. Last week, he unveiled a website aimed at raising the virtual currency’s public profile. Some foundation members are dismayed by Matonis’ leadership and grander plans.

Investors from Silicon Valley, in particular, would like the group to focus on more technical matters, particularly fortifying the underlying bitcoin software so it can grow into a viable, large-scale payment network.

Running the foundation is like “going downhill in a go- cart trying to keep the wheels on,” Matonis said. “There are different constituencies going in different directions.”

Venture capitalists and entrepreneurs, lured by the technology’s promise, have ploughed time and money into bitcoin businesses – and they’re demanding software upgrades to develop the digital currency’s commercial potential.

“The impact of the bitcoin protocol is economic,” Jeremy Allaire, chief executive of Circle Internet Financial, a bitcoin start-up. “These are higher stakes than with other open-source software.”

The organisation, established in 2012 and modelled on the Linux Foundation, the open-source operating system created in the early 1990s, has tried to mix stewardship of the code with political advocacy. Digital assets

Unlike Linux, bitcoin rapidly became a channel for billions of dollars in transactions, making security and capacity bottom-line issues for entrepreneurs.

Matonis said that pressure to invest more in bitcoin’s computer code reflects a “fight over who controls the policy dialogue”, and whether the group will continue to fund lobbying. “Tech investors want to make sure that all the resources in the world are there on the tech side,” he said.

Bitcoins are part of a software system that transfers digital assets from owner to owner without using a third party. Start-ups are seeking to use the innovation to disrupt the existing payment system dominated by firms such as JPMorgan Chase, Visa and Western Union.

The core software managed by the foundation contains instructions that let computers communicate with one another to verify transactions on bitcoin’s public ledger, called the blockchain.

Another program enables users to conduct those transactions. Software upgrades are made through an informal system of mostly part- time developers who communicate in internet chat rooms.

Gavin Andresen, the foundation’s chief scientist, was until May the only paid coder working on bitcoin. Online discussions sometimes devolve into virtual shouting matches, according to Andresen.

This year, the bitcoin network processed between $20 million and $580 million per day in transactions, according to the data aggregated on blockchain.info.

“This is not sustainable,” said Mike Hearn, one of bitcoin’s core developers. “You can’t have an infrastructure held together by chewing gum and sticky tape and people who work evenings and weekends.”

Software upgrades have helped ward off hacking and increased commercial utility. A change in March, for example, improved the security of transactions conducted through online merchants by adapting bitcoin software to the Internet’s existing system for authenticating websites.

That tweak pales in comparison to the “non-trivial problem” of raising the number of transactions the bitcoin network can process, Allaire said. The system can handle about nine transactions per second, far off the roughly 2,400 on Visa’s network. Investors have raised the idea of earmarking donations to the foundation for work on the software.

“A lot of people would give a million dollars if it would go solely to development,” said Brock Pierce, a venture capitalist who was recently elected to the foundation’s board. Under pressure from the entrepreneur side, the foundation has commissioned a “feasibility study” to determine whether the software development could happen as part of a partnership with a major university, Matonis said.

Digital wallets

“If we don’t have the underlying core development, it diminishes the other policy and advocacy work we do,” he said. Matonis has frequently argued that bitcoin is a political project that will displace money issued by governments, and has at times disavowed close work with regulators.

“The foundation is not pro-regulation as some have claimed, but it is pro-education,” he wrote when he became its director in 2012. He has dismissed money laundering as an overly broad category of crime, “like buying a drive-thru donut in a stolen vehicle”.

Many entrepreneurs are keen to dodge the politics that Matonis courts. Nic Cary, the chief executive officer of Blockchain, the largest website for creating digital wallets to hold bitcoins, said the group should improve software and promote consumer adoption of the virtual currency.

“What we’ve seen is a lot of mission creep,” Cary said. “We need to fund the people who are working on development.”

Matonis and the other founders of the group have rules on their side. They set up a system in which individual members elect the same number of board members – three – as do all the corporate members. That has raised the possibility, mentioned by Matonis at a meeting in Amsterdam in May, that the foundation could split. The Electronic Frontier Foundation, an early Internet advocacy group, spun out the Washington-based Center for Democracy and Technology in 1994 after similar conflicts.

Matonis told his members that he won’t go quietly if the Bitcoin Foundation cracks. “If we’re going to fracture,” Matonis said in May, “I want to make sure I’m running the one we remember.” – Bloomberg

Crypto-anarchy is not some crazy utopian ideology, but a very viable thing that unfolds in front of our eyes this very moment. The Internet and Bitcoin will soon allow people solve social problems in a novel way: instead of ancient formula “the strongest wins and beats the shit out of the loser” we all can achieve a peaceful society where both rich and poor, strong and weak can protect their property and freedom on more equal grounds without relying on violent institutions like governments.

But first, lets start with some history.

Cypherpunk movement started as a mailing list in 1992. In 1993 Eric Hughes publishes a “A Cypherpunk’s Manifesto” [1]. In 1994 Timothy C. May publishes “Cypherpunks FAQ” [2].

Here’s an excerpt from the FAQ:

2.3. “What’s the ‘Big Picture’?”

Strong crypto is here. It is widely available. It implies many changes in the way the world works. Private channels between parties who have never met and who never will meet are possible. Totally anonymous, unsinkable, untraceable communications and exchanges are possible.

Transactions can only be voluntary, since the parties are untraceable and unknown and can withdraw at any time. This has profound implications for the conventional approach of using the threat of force, directed against parties by governments or by others. In particular, threats of force will fail.

What emerges from this is unclear, but I think it will be a form of anarcho-capitalist market system I call “crypto anarchy.” (Voluntary communications only, with no third parties butting in.)

In 1994 Nick Szabo coins the term “smart contract” [3] and describes all use case categories that are talking about today: from digital cash to synthetic financial assets and smart property.

In 1998 Wei Dai & Nick Szabo came up with the ideas for “b-money” [4] and “bit gold” [5] during their conversation on the libtech-l mailing list. Wei Dai captured the essence of the movement in an immortal quote:

I am fascinated by Tim May’s crypto-anarchy. Unlike the communities traditionally associated with the word “anarchy”, in a crypto-anarchy the government is not temporarily destroyed but permanently forbidden and permanently unnecessary. It’s a community where the threat of violence is impotent because violence is impossible, and violence is impossible because its participants cannot be linked to their true names or physical locations.

In 1999 Nick Szabo coins term “intrapolynomial cryptography” [6] for the entirety of proof-of-work algorithms and describes what we call now a “private blockchain”, a chain of property ownership enforced by a consensus of “property club” members [7]. The latter article is especially valuable today as it explicitly states that the job of voting in the consensus mechanism is used only for secure execution of the agreed-upon rules and database replication, but not for changing the rules themselves.

In 2004 Hal Finney implements a RPOW server [8] (“Reusable proof of work”) inspired by the bit gold proposal. The RPOW scheme uses a secure processing module that simultaneously acts as a mint and as a custodian for the ledger of proof-of-work tokens.

In late 2008 Satoshi Nakamoto publishes an overview of Bitcoin [9] and on January 3rd, 2009 releases the code and begins the blockchain.

Bitcoin is the exact implementation of the system envisioned by Tim C. May, Wei Dai and Nick Szabo. The only requirement is for transacting parties to remain anonymous. If there’s no trace to physical persons, there is no place for the violent intervention and thus the contracts can only be enforced according to the voluntarily agreed-upon rules between the parties. Bitcoin allows encoding these rules right in the transactions so they are automatically enforced by the whole network.

In practice, we cannot imagine living in full anonymity. Human beings live in a physical world and enjoy a lot of physical things. Anonymity is not something you can easily manage like a single encryption key. It must be maintained via careful dissemination of one’s actions among actions of others. And since the network activity is easily recordable, one mistake is enough to reveal oneself. In other words, the cost of anonymity is rather high compared to the benefits. Does this mean crypto-anarchy is an utopia?

I would argue, it’s far from it. Cypherpunks being rigorous scientists made a much stronger assumption than needed in practice. For transacting parties it is enough to have costs of cheating (e.g. resorting to violent coercion) meaningfully higher than the cost of following the contract (that is, keeping the promise). If that condition holds for the majority of interactions in society, there will be a great incentive for people to protect themselves against remaining rare cases of cheating thus keeping the system sustainable. Anonymity is simply one of the ways to raise the cost of the attack.

Bitcoin raises the cost of many kinds of attacks, going far beyond protecting against central banks meddling with money supply.

First, all sorts of computational services will flourish. Machines never need to disclose their physical locations and can freely automate both payment verification and payments themselves. Denial-of-service and spam can be largely eliminated by simply requiring a smallish payment for every request.

Second, personal services can be protected by peer-to-peer insurance deposits [8] that literally raises the cost of cheating by making both parties agree to a greater sacrifice (“bilateral insurance deposit”).

In a similar manner, crowdfunding can be fully insured by allowing raised funds to be reverted if the majority of shareholders decides to do so.

Finally, systemic predation by the state becomes economically impossible. Most modern states fund themselves by debasing money supply (also known as “bond issuance”, “budget deficit”, “inflation”, “quantitative easing”, “stimulus package”). Bitcoin-based economy simply does not allow this as it is very cheap to store bitcoins and verify transactions yourself and completely avoid all kinds of fraud associated with modern banking. As central banking disappears from the state’s arsenal, federal government activities including wars become unfunded and quickly come to an end.

Local governments may continue their operations funded by local taxes, but that would become increasingly voluntary. Extracting bitcoins costs much more than protecting them. There is no highly centralized and monitored banking network, so it’s much harder to track taxable transactions. Every additional tax evader defunds the local police department and makes it safer for the next person to underreport earnings if he wishes to do so. Considering that the law enforcement is paid only a small portion of the total budget to be extracted (50% goes to bureaucrats and the rest to other public services), consistently extracting bits of information from millions of individuals is unsustainable in the long run. If anyone is good at stealing bitcoins, they are much better off doing it alone and taking all profits for themselves.

Governments, of course, can also tax in kind (like your underreported Ferrari or a house), but this would be even costlier than seizing any kind of money and those costs must be paid by the state in bitcoins that it does not have to start with.

If this speculation does not sound to you like a complete lunacy yet, here is the fun part. Most governments are completely broke already and can only pay with the IOUs they print. When people start a massive run for bitcoins to protect their wealth, everyone will be able to earn bitcoins for their work, except those who work for the government. Policemen, public school teachers and alike will be the first ones to notice prices rising faster than their salaries. They will be the first ones to switch jobs or become largely corrupt on all levels, like it was in Russia after the fall of the Soviet Union. Bureaucrats will smell the approaching panic and, instead of trying to retain control over the employees, will privatize as much public goods as possible. Again, exactly like during the fall of the Soviet Union. People will see how all promised public services are either abandoned or stolen, and this time everyone will have a method to protect their own property and do business voluntarily and in an even safer and cheaper way than before. Crypto-anarchy will quickly become a boring reality without the need for anyone to remain fully anonymous.

The average size of a block is approaching the 1 MB protocol limit for the first time in Bitcoins history, and not everybody agrees regarding what to do about it. Many objections to raising or removing the block size limit are based on misunderstandings about the nature of economic scarcity and operation of markets in general.

ECONOMIC FALLACIES AND THE BLOCK SIZE LIMIT

This is the first article in a series about the economics of the Bitcoin protocols block size limit. This article covers scarcity. The second article covers price discovery and the third article will cover why the block reward is fundamentally different than the block size.

Production Quotas

As you may have heard, Bitcoin usage is growing. In every way, that graph represents the kind of healthy exponential adoption that we all want to see.

Unfortunately there's a problem on the horizon which threatens to stop or even reverse Bitcoin adoption.

Several years ago, Satoshi added a protocol limit to the maximum size of a Bitcoin block. Prior to this change, there was no explicit limit, just an implicit 32 megabyte maximum message size. This limit was explained as a temporary anti-spam measure, and Satoshi said at the time that it could be raised when the network needed the additional capability.

The economic effect of having a maximum block size is that of a production quota. Production quotas are tools of economic central planning that either mandate or limit the amount of production of a good or service, as opposed to allowing the production rates to be governed by supply and demand.

Production quotas are inherently harmful to an economy, as shown in the 1920 essay, Economic Calculation in the Socialist Commonwealth, and so do not represent a sustainable long term strategy for allocating the supply of Bitcoin transactions.

From the time it was implemented until now, the harm caused by the block size limit has been hypothetical rather than real since there has not yet been enough demand for Bitcoin transactions to be hampered by the limit. For the last few years, the block size limit has been like a minimum wage law that forbids salaries lower than $0.01 per year. There is no market demand for salaries that low, and so such a minimum wage law might as well not exist it has no effect on the economy. Likewise, the 1 MB block size limit has not yet had any effect on the Bitcoin economy since there has not yet been a market demand for more than 1 MB of transactions every 10 minutes.

Since its inception, Bitcoin has been operating as if there was no block size limit at all. If this limit is kept in place when the market demand for transactions rises above 1 MB/10 minutes, then suddenly Bitcoin will be in uncharted economic territory.

People will want to use Bitcoin, but they will be forbidden by protocol from doing so. No matter how much they are willing to pay, no matter how willing miners are to include their transactions in a block, no matter how willing the full node operators are to forward their transactions, they simply wont be allowed to transact.

A block size limit that is low enough to have a real effect on actual block sizes is the ultimate blacklist.

The Alternative to Central Planning

The best alternative to a production quota on Bitcoin transactions is, like in any other situation of central planning, to allow the market to decide the optimum block size.

Nobody gives McDonalds a maximum number of Big Macs they are allowed to produce each day their customers tell them how many they want to buy and McDonalds responds appropriately. At any given time, there exists a price at which the willingness of McDonalds to produce Big Macs is exactly equal to the willingness of their customers to buy them, and that determines the number that will be produced. The process of price discovery is an emergent property of the actions of millions of independent actors expressing their preferences in a competitive open market.

This is exactly how we want Bitcoin to behave. The Bitcoin network, like any other product or service in the economy, should change its production capability to respond to supply and demand.

It is not currently designed to do this, however, and one of the barriers preventing Bitcoin from being improved in this way is a series of economic fallacies or misconceptions that cause otherwise skilled people to distrust market-driven price discovery over central planning, or to assume that resource allocation in computer networks operates in a manner fundamentally different than resource allocation in any other part of the economy.

Objections to Market-Determined Block Sizes

"Transaction fees are too low and won't rise unless space in a block is scarce. We need a block size limit to ensure block space scarcity and thus price transactions."

This objection is based on a common misunderstanding of the word scarcity as it applies to economics.

In economic terms, something is scarce if people cant have an infinite amount of it at a price of zero.

On the surface of the Earth, air is not scarce. Its not scarce because every human can breathe as much as they are capable of breathing, without paying for the air, and theres still enough to go around. Because everybody can consume as much as they are capable of without reducing anyone elses ability to do the same, air does not require allocation. In practical terms, the amount of available air at a price of zero is infinite, therefore air is not scarce.

Almost everything else is scarce, certainly any services that require time and/or energy to produce.

The space in a block will always be scarce as long as our computers are still made of matter and still occupy space. Constructing a block isn't free, storing a block isn't free, and the bandwidth needed to transmit a block is not free.

There will always exist some cost to a miner to add a transaction to a block. That cost may be very small, but it will never be zero.

If transaction fees emerge from the operation of a competitive open market, then we would expect them to approach the marginal cost of production, plus a small profit margin.

What if the the market-set block size is so big that only Google can afford to run full nodes?

This is a real problem that could emerge, and is actually the reason that the block size limit was enacted in the first place.

The reason this could happen is because of poor P2P network design: miners do not need to pay the cost of relaying blocks throughout the network, therefore this cost becomes an externality which is not reflected in their marginal cost of production.

The solution to this objection is a better P2P network design, not a production quota that limits the maximum transaction rate.

A description of how to build a better P2P network will be the subject of a future article.

What if the market-set transaction fee doesn't pay enough for a hash rate that protects the network for well-funded adversaries?

If there is not enough market demand for Bitcoin transactions such to pay for sufficient hashing power to protect the network, then Bitcoin will fail.

This will happen with or without a block size limit.

Since its inception, Bitcoin has been on a collision course with extremely well funded, entitled, and politically powerful interests. Its only hope of surviving this collision is by attracting a very broad base of support.

Bitcoin needs millions, and then billions, of users who demand better money. The demand for Bitcoin must be strong enough that they will break the law if that's what it takes to obtain it.

The above strategy isn't particularly novel or extreme this strategy has been employed in the conflict between peer-to-peer filesharing networks vs the copyright mafia, and more recently by ridesharing companies vs the taxi licensing cartels.

When a new technology has to compete against entrenched interests on a non-level political playing field, civil disobedience is a proven effective tactic.

We don't yet know whether or not Bitcoin will gain enough of the right kind of support it needs to survive.

We can say, however, that arbitrarily rationing the transaction rate is counterproductive toward achieving that end.

What if competition results in the profitability of mining being so low that it drives out smaller pools and Bitcoin mining converges to a monopoly?

This objection is a restatement of the natural monopoly argument, and is in no way specific to Bitcoin.

Natural monopoly as an economic theory has been conclusively debunked, and the same principles that explain why natural monopolies do not emerge from free market forces in classically-cited industries apply equally well to Bitcoin mining.

Rather than repeat those arguments here, anyone who is concerned about natural monopolies should read The Myth of Natural Monopoly by Thomas J. DiLorenzo.

If the market should set the block size, why shouldn't it also set the block reward?

This objection is based either on a fundamental misunderstanding on the nature of money, or else on the misconception that Bitcoins value is not derived from its monetary properties.

Exploring these misconceptions fully will be the subject of a future article.

This concludes part 1. Future articles in this series will address the subject of how to build economically-scalable P2P networks, and why the block reward is fundamentally different than the block size limit.

I am an e-Money researcher and a Founding Director of the Bitcoin Foundation. My career has included senior influential posts at Sumitomo Bank, VISA, VeriSign, and Hushmail.

"Free-market protagonists, such as Matonis, regard cybercash as better than traditional government-issued or -regulated money, because it is determined by market forces and thus nonpolitical in nature." --Robert Guttmann, Professor of Economics at Hofstra University, in Cybercash: The Coming Era of Electronic Money, 2002

"Matonis is quite correct that the new technology makes easier the use of multiple private currencies." --Mark Bernkopf, Federal Reserve Bank of New York, in "Electronic Cash and Monetary Policy", 1996

"Matonis argues that what is about to happen in the world of money is nothing less than the birth of a new Knowledge Age industry: the development, issuance, and management of private currencies." --Seth Godin in Presenting Digital Cash, 1995